If you’re a business owner, borrowing money may have crossed your mind at some point. Debt can help launch a business, expand it, or help it survive through difficult times. But it’s understandable if the fear of missing monthly payments or drowning in interest fees prevents you from taking on business debt.

While debt often has negative connotations, there are certain situations where debt can be a good thing, if you know how to leverage it.

**Now, before we get into things, keep in mind that I’m not a financial advisor. I can’t tell you that debt is something that you personally should take on, or that it’s best for your situation. But I can tell you, as someone who has used debt before myself, that in some cases, it can be useful, but that will depend on your situation. It’s always a good idea to consult with a financial advisor before taking on a substantial amount of debt for your business.**

In this article, we’ll be tackling some of the big questions you might have about borrowing money for an ecommerce business, such as: What are the benefits of borrowing money for a business? How much debt is too much? And what are some examples of good and bad business debt?

Let’s dive in.

Differences Between Good and Bad Business Debt

While fundamentally, you might say that all debt is the same. After all, debt is money that’s borrowed now to be paid back at a future date, often with interest. However, not all debt is created equal. Whether debt is considered good or bad will depend on a few different factors surrounding the debt in question: namely, is it something that will help you to grow your business, or just money down the drain.

These factors include things like your financial situation, the type of debt you’re taking on, what you’re using the money for, and the level of risk involved. The consequences of the debt also determine whether it’s good debt or not. Debt can potentially increase your bottom line or it could be a waste of money. To get positive outcomes with debt, you have to know the difference between good and bad business debt.

Below is a quick overview of the main differences between good and bad debt.

Good debt:

- Increases your net worth

- Increases your business’ net worth

- Brings future value

- Often, low interest

While bad debt:

- Decreases your net worth

- Results in business losses

- Involves purchases that are perishable or lose a great deal of their value over time

- Often, high interest

Debt Financing vs. Equity Financing

(Source: Shutterstock)

While there are dozens of ways to structure financing, they really come down to two categories: debt financing and equity financing. Some companies may do a combination of both. Each has distinct advantages and disadvantages that should be considered beforehand.

Equity financing raises capital through the sale of shares. It provides businesses with extra working capital without a repayment obligation. It doesn’t place an additional financial burden on the company, but the trade-off is that you give a portion of company ownership to the lenders and they become equity holders.

Debt financing on the other hand is when a business borrows money from individuals or a financial institution. Debt financing comes with an obligation to repay the full amount plus interest. It doesn’t require a company to give away ownership stakes. New and small businesses often rely on debt financing to raise funds to grow their business.

Choosing between the two depends on which source of funding is accessible for your company, its cash flow, and how important ownership and maintaining control are to you.

In the next section, we’ll look into some examples of good and bad business debts.

Examples of Potentially Good and Bad Debt for Your Ecommerce Business

Here are a few signs that it might be a bad idea to take on debt for your business:

- It’ll increase my gross profit

- It’ll be used for expenses (With no solid plan to pay it back)

- It’ll be used for inventory (With no solid plan to pay it back)

- It’s got a high-interest rate, but it’s all I qualify for right now

Here are some situations where it may make sense to take on debt for your business:

- This debt is being taken on after being honest about my historical numbers and realistic about future projections, taking into consideration marketplace unknowns and variables

- The debt will be used for acquisitions which will increase our overall cash flow and/or will add value to the existing business

- I’ll use the funds for the inventory, however, there is enough profit margin to cover the cost of the loan and pay it back (While still making a profit)

- The loan has a reasonable interest rate; the only exception to paying a high-interest rate is if it is a bridge loan, or if you have an exit strategy that would provide a greater rate of return

Examples of Business Loans

Kenneth Hearn, fund manager at SwissOne Capital AG, describes good debt as money borrowed to pay for items that will contribute to the growth and development of a business. He tells the US Chamber of Commerce, “A general rule of ‘good debt’ is debt that is low-interest, or will increase the overall net worth of your business.”

Here are some examples of loans that are available to businesses:

Commercial Mortgage Debt

These are loans made by businesses that want to purchase properties. This allows businesses to own their own land, office space, building, or warehouse without having to pay all the costs up-front. The value of property tends to increase over time, so it’s considered a good debt with value for the long term.

Term Loans

Term loans are available at banks or credit unions. These are one of the most common loans available to small businesses and can be used for anything from equipment to inventory. With term loans, the monthly payments are usually fixed, making repayment easier to budget for.

Whether this debt is good or bad will depend largely on what it’s used for and the success of the investment.

Government-Backed Loans

These loans subsidized by the government provide capital for businesses looking to get affordable funding options, and include Small Business Administration (SBA) loans. Compared to other debt financing options, repayment terms on government loans may be easier to manage. Some of these loans may allow interest-only payments for a certain period of time. Government loans may also have more affordable interest rates than a regular bank loan or other financing options.

As with term loans, government-backed loans may be a good form of debt, but this will depend on how well it’s leveraged.

Business Credit Cards

Credit cards are tricky. If you know you’ll be able to pay your debt in full each month, credit card debt can be a good way of raising funds, especially for new business owners who may not have a business credit standing yet but need cash quickly. It’s also interest-free IF you pay on time.

The big caveat to credit cards is that if you don’t pay the total balance at the end of the period, the interest (often high) adds up, creating unmanageable debt. There are also negative impacts on your personal credit score and business credit score if you use too much available credit or fall behind on the payments.

Business Line of Credit

This is a type of revolving credit and works like a business credit card. Interest rates on a business line of credit are usually higher than on term loans or an SBA loan. You can build better business credit by paying on time and having a good line of credit. However, failure to manage this type of financing can easily lead to bad debt.

Merchant Cash Advances (MCA)

With merchant cash advances, business owners receive a lump sum payment. Loans are repaid with future credit card sales. This type of debt financing works if you expect to see an increase in revenue over the next few years. Merchant cash advances are helpful to borrowers with bad credit. However, its expensive processing fees can make your business’s financial situation worse in the long term.

Short-Term Loans

Short-term loans include payday loans, business cash advances, and cash flow loans. These are loans taken out by business owners that need cash quickly, with the debt expected to be paid back within a month. These loans can be very attractive because of their low barriers to entry. They also rarely have credit requirements.

However, they often have very high interest rates, making it difficult for struggling businesses to stay on top of payments. If you accrue a lot of debt, some lenders may also use unethical practices to collect, such as using threats and aggression or taking money directly from your bank account.

Get our GN -Good Debt Vs. Bad Debt for Business delivered right to your inbox.

Borrowing Money for a Business

Lyle Solomon, principal attorney for Oak View Law Group, warns business owners about “predatory loans” such as cash advance loans and payday loans. Solomon tells the US Chamber of Commerce, “These loans target people with bad credit or low income with few options to consider. They often come with exorbitant interest rates and unethical terms.”

Solomon has advice for business owners: “Healthy debt entails borrowing money for investing in items that do not depreciate over time. Try to use the funds to reduce a loss or catastrophe.” Even with debt, your business can still be profitable, as long as you invest it in business assets that lead to growth.

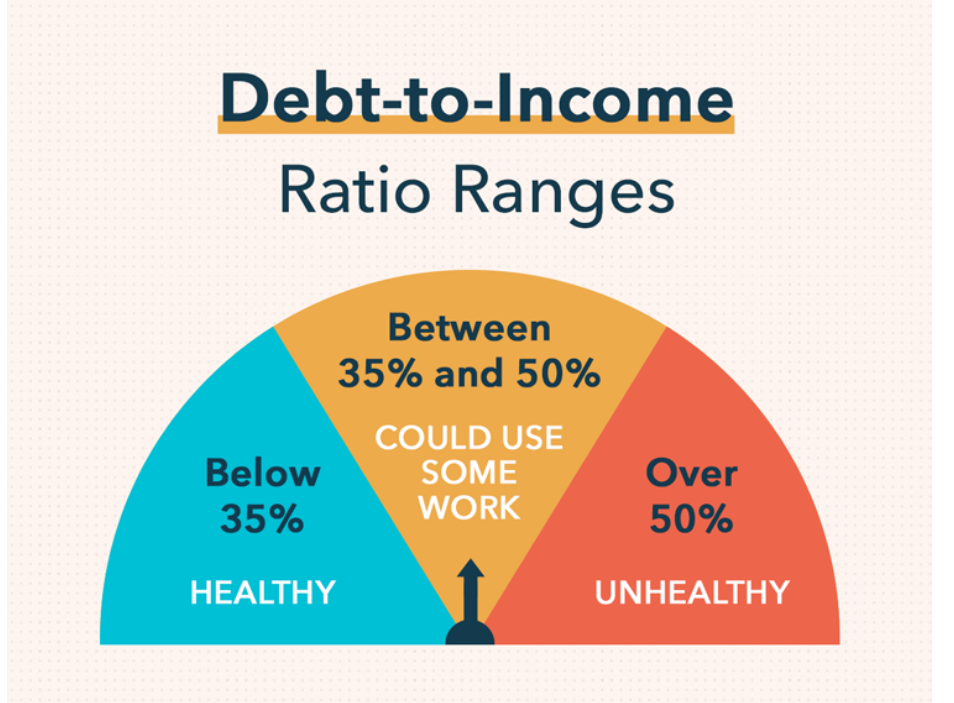

How do you know if your business has too much debt?

The debt-to-income ratio (DTI) tells you whether or not you have too much debt. Wells Fargo defines DTI as a ratio that compares how much you owe each month to how much you earn. It can help you determine how comfortable you are with your existing debts and helps you decide what type of debt is the best for you.

To get this value, add all of your monthly expenses, then divide the total by your monthly income. You can also use this Debt-to-Income Ratio Calculator from Wells Fargo:

(Source: Intuit)

How much debt should you take on when starting a business?

Sean Salas, CEO of Camino Financial, has great advice on this: “A small business owner should never take on more debt than the business can pay back. For instance, a small business should only take on $1 of debt (and interest obligations) for every $1.25 the company generates in cash, leaving the business with enough cash flow cushion to pay off lenders during downtimes. With the right balance of debt and equity, small business owners can optimize the cost of the firm’s capital structure.”

How do you combat bad debt?

Sometimes, a sudden sales slowdown can put pressure on a company’s capacity to keep up with loan payments. If this happens, here are some tips on managing bad debt:

- If you have several loans, it’s important to prioritize which ones to pay off first. Start with the ones with the most serious consequences such as high interest rates or concerning conditions hidden within the terms of the loan.

- Use your negotiation skills to adjust the terms and conditions of your bank loans. You can also ask if they offer alternative payment plans or loan restructuring.

- Look for ways to increase your ecommerce business sales. Use strategies that increase a customer’s average order value or run a special sale to encourage turnover.

(Source: Shutterstock)

Should You Take On Debt?

At the end of the day, it’s always best to test out your idea first. Run through the process, use your own funds when possible, and start on a small scale to test the waters and gauge interest, demand, and profitability. Then, once you start to turn a profit, you can feel more confident about whether your idea is one that would benefit from additional funding.

It’s also all about what your big-picture goals are like and how comfortable you will be having a certain amount of debt hanging over your head.

And of course, as always, be sure to consult with a professional financial advisor or run your ideas by someone in your space who’s been there, done that, and who understands how debt works. They can help you to see whether or not the numbers check out and if taking on debt right now is a good idea.

Remember, you shouldn’t wait until you need money to go look for it. I always recommend that businesses open up a line of credit as quickly as they can, so they have it available should they ever need it. If you wait until you truly need the loan, whether due to a slow down, a need for more inventory, etc., usually it means the financials of the business might not be strong enough to qualify for one.

FAQs on Debt For Small Ecommerce Businesses

Here are some frequently asked questions about debt for ecommerce businesses:

Is a business loan good or bad debt?

Debt in itself isn’t good or bad. What ultimately makes it bad or good are the circumstances that surround it: your financial situation, purpose for borrowing money, the loan’s interest rate, repayment terms, and outcomes on your business’s net worth.

How much debt is normal for a small business?

A small business’s debt-to-income (DTI) ratio is a good indicator of how large a company’s debt is relative to its income. A lower DTI means that a business has more cash flow. If a considerable amount of money goes into paying off debt rather than investing in the business, that’s a sign that a business has too much debt.

What are the three C’s of credit?

Your credit score, or the measure of factors that reflect your ability to pay off a loan, is determined by the three C’s of credit: Character, Capital, and Capacity.

The Next Steps: How to Choose the Right Debt

Do you feel like a loan could help your business? Make sure you do these things first:

Step One: Define your desired outcomes for the debt. If you borrow money without a clear purpose, debt can quickly go from good to bad. Set your goals then define the metrics that will show you if your debt is bringing you closer to your financial goals. Make sure you’re not blindsighted by your hope that your business will succeed, instead, make sure you take the time to create accurate projections based on solid data. If you’re stuck, consider having a second pair of eyes look at your plans as well.

Step Two: Look at your financials and sales forecasts. Business plans and financial statements aren’t just for the lenders. As a borrower, knowing your business’s current financial standing and sales forecasts will help you see if you’ll be able to realistically pay off debt.

Step Three: Read the fine print. Understanding all the terms and conditions ensures that you’re not going to get into overwhelming interest expenses in case you miss a monthly payment.

Business debt isn’t always bad. With careful planning and management, debt financing can be a great tool to boost your business’s growth and profitability. But misused, it can have serious consequences on your business. Before you get a loan, it’s important to understand the differences between bad and healthy debt so that you can use it to your advantage.

Looking for effective strategies to scale your ecommerce business? Reach out now for your FREE 20-minute consultation call. Let’s find the best solutions to help your company grow fast.

Get our GN -Good Debt Vs. Bad Debt for Business delivered right to your inbox.